The graphic above (click to enlarge) shows four alternative futures for US1, an index of overall growth in the US SocioEconomic System (see the measurement matrix below). It is based on computer simulations of alternative estimated state space models. I would argue that the graphic says a lot about why US voters decided the way they did in the 2024 Presidential Election and what we can expect from the new, Right-Wing Republican Administration after 2025.First, why did the MAGA movement embrace an extension of the American First isolationist movement? The Foreign Policy of the Obama Administration (2009-2017) was directed toward the World System and was not Isolationist. The World System input model (W) in the graphic above put the US on a slower overall growth path (dotted green line). I would argue that voters were well aware that growth of the US Economy and the US standard of living was slowing (see Economist Kathryn Ann Edward's comments here). The realization led to a Right-Wing backlash (the same thing that happened in Germany during the Inter-War (WWI-WWII) Years, see Arno Mayer's The Persistence of the Old Regime).

Second, the President-elect's policy pronouncements and transition plans suggest abandoning the World System and doing everything possible to stimulate unlimited endogenous economic growth in the US: eliminating regulation, ignoring white-collar crime, closing borders to immigrants, abandoning environmental regulation (allowing businesses to exploit free environmental resources), eliminating labor regulation (a restraint on profits), dismantling the Welfare State, slashing business taxes (another restraint on profits), eliminating funding for and control over education (a stimulus to wage growth and a limit on profits), etc.

The red and the blue dashed lines in the graphic above show possible time paths for the US Economy unleashed. The models predict uncontrolled, unending exponential growth for the US System. They are, I would argue, a business man's fantasy. Nothing can grow forever and eventually limits will be reached (my models suggest sometime after 2050). Most of us living at the present moment, me included, will be dead by then. It will be someone else's problem.

There is another possible time path for the US SocioEconomic System: the Random Walk (RW, the solid line in the graphic above). No one can know the future. Attempts to dismantle failing US Institutions may or may not happen as imagined. The new Administration's cabinet picks, so far, are not reassuring. Essentially, in a Random Walk, today is like yesterday except for random error, actions by people who are making it up as they go along.

I am always surprised that commentators can seem so confident about what happened in the 2024 Presidential election and what will happen as a result of it. I'm not. My advice for the future is to take defensive positions and not follow Economic Bubbles that might develop in response to crippling of US regulatory institutions.

We know our current systems are failing and need to be rebuilt. In future posts I will look more carefully at all of these systems.

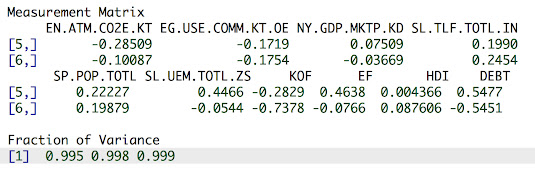

US Measurement Matrix

The graphic at the beginning of this post applies the weights from row [1,] of the state space measurement matrix to 36 indicators of US development from 1950-2010. After 2010, the results are simulated from four state space models: RW (Random Walk), W (World System input), US (components from rows [2,] and [3,] in the measurement matrix), and BAU (a Business as Usual model with no inputs).

Measurement Matrix

L.US.E. L.US.U. GDP.US. GDP.C. GDP.I. GDP.X.

[1,] 0.1955 0.138 0.1978 0.1972 0.1961 -0.1402

[2,] 0.0669 0.200 -0.0462 -0.0554 -0.0355 0.0751

[3,] -0.0312 0.239 0.0284 0.0314 -0.0272 0.2229

GDP.G. P.US.TBILL. P.CPAPER. P.FED.FUNDS. P.CPI.

[1,] 0.1976 0.00429 -0.01554 0.0127 0.19773

[2,] -0.0377 0.40583 0.40460 0.3998 0.00996

[3,] 0.0541 0.07630 -0.00165 0.0986 0.02128

P.GDP. P.SP500. V.NYSE. P.S.P.DPR. P.S.P.EPR.

[1,] 0.1967 0.1868 0.166 -0.146 -0.112

[2,] 0.0337 -0.1076 -0.131 0.144 0.128

[3,] 0.0240 -0.0277 0.165 0.321 0.384

Q.H.Starts. K.US. M1 M2 P.WPI. Q.A.

[1,] -0.0202 0.1974 0.1953 0.1979 0.1932 0.1918

[2,] 0.0392 -0.0418 -0.0145 -0.0325 0.0612 0.0766

[3,] -0.4666 0.0446 -0.0318 0.0472 0.1051 -0.0973

Q.I. O.B. P.FUELS. P.W.AG. P.W.MFG. Q.OIL.

[1,] 0.1967 -0.173 0.1834 0.1983 0.1990 -0.113

[2,] 0.0374 0.186 0.0269 0.0131 0.0125 0.312

[3,] -0.0683 0.110 0.2538 0.0489 0.0232 -0.145

N.US. IMM.US. U.US. CAPU EF Globalization

[1,] 0.1951 0.1440 0.1967 -0.141 0.1867 0.0818

[2,] 0.0746 0.0546 0.0477 -0.153 0.1096 -0.2964

[3,] -0.0642 -0.1371 -0.0589 -0.164 0.0303 0.3905

CO2 Q.FOSSIL.

[1,] 0.180 0.129

[2,] 0.155 0.283

[3,] -0.110 -0.157

Fraction of Variance

[1] 0.698 0.854 0.900

Atlanta Fed Economy Now

Hurricane Forecasting

My vision for SocioEconomic system forecasting is to follow the US National Oceanic and Atmospheric Administration's (NOAA) approach to hurricane (Economic Crisis?) forecasting using Spaghetti Models (see below). Currently, Economic forecasting does not use Multimodel Inference but it is getting there! The best state space model for the US SocioEconomic System in the graphic at the beginning of this post is the World System (W) model based on the AIC Criterion.

Climate Change

Another comparison for what I have presented above are the IPCC Emission Scenarios. These scenarios are for the World System. Needless to say, the new Right-Wing Republican administration plans on withdrawing the US from all attempts to study or ameliorate Climate Change.