What is somewhat confusing about all this is that there is a branch of Economics called Modern Monetary Theory (MMT) that suggests that there can be no debt crises when governments control their own currency, as do the governments in the US, France, Germany and Canada. Populist Deficit Hawks argue that everyone understands that we can accumulate too much debt and wind up in bankruptcy. MMT counters that if individuals go into too much debt they cannot simply print money to get out of debt as modern governments can. As long as there are slack resources in the US Economy, government deficit spending will not create inflation. If you are not familiar with the theoretical arguments, the controversies make interesting reading (here and here).

From the perspective of Systems Theory, Debt Crises reveal yet another Error Correcting Controller (ECC) that is being used to control outputs of the Political System. Regardless of theoretical and rational considerations, the DEBT ECC triggers an important feedback loop we need to understand. If governments have to go into debt to address the Climate Crisis or any other of the many Overlapping Crises, ideas about DEBT will assert themselves as a constraint on spending.

In the graphic above, I have displayed a history of US Debt from 1970 to the present and a forecast for the future out to 2060 by political administration. Debt has been fairly close to the (increasing) attractor path except during the Clinton Administration when it went down, during the Obama Administration when it went up and during the Trump I Administration when it went way up (above the 98% prediction interval) as a result of the COVID-19 Pandemic. The USL20 model's forecast for the future is that US Debt will be declining but with rather wide prediction intervals. Given the historical data, almost anything can happen.

Notes

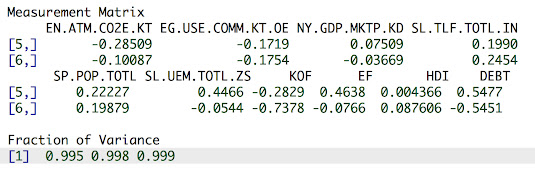

Data are taken from the World Development Indicators (WDI). All variables are in standard scores. The methodology used to create forecasts is similar to the one used by the Atlanta Federal Reserves GDPNow app. Prediction intervals are generated using a Bootstrap algorithm in the R programming language. The Akaike Information Criterion (AIC) is used for model selection.